Overview

Bridging loans and traditional term mortgages are two common ways of financing property purchases in the UK, but they cater to different situations. A traditional term mortgage is the standard choice for long-term homeownership or rental investment. Bridging loans, on the other hand, are fast, short-term funding options used when time is critical or the property doesn’t yet qualify for a term mortgage. In 2025, bridging finance has become more mainstream, supporting everyone from first-time buyers to experienced developers. This guide compares how both options work and when each one might suit your needs.

What Is a Bridging Loan?

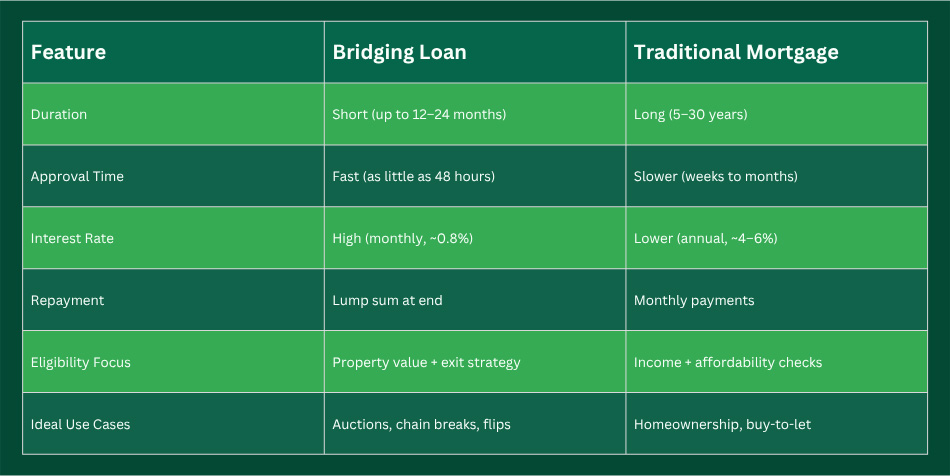

A bridging loan is a short-term loan secured against property. It helps people access funds quickly – usually to buy a new home, secure an investment property, or finish a development – while they wait for longer-term finance or a property sale. Bridging loans typically last from a few weeks to 12 months, sometimes up to two years.

Bridging finance is often used:

- To buy a new property before your old one sells

- For auction purchases needing fast completion

- For buying and renovating properties not yet mortgageable

- To repay development finance while waiting to sell completed units

Interest is charged monthly (e.g., 0.5% to 1.5%) and is repaid at the end in one lump sum, often alongside the loan amount. This makes bridging helpful for short-term use but costly if held too long. Approval focuses more on the property’s value and a clear exit strategy rather than income or credit score.

What Is a Traditional Term Mortgage?

A traditional term mortgage is a long-term loan used to purchase or refinance a property. It usually runs over 25 to 30 years and is repaid through monthly instalments, either on an interest-only or capital repayment basis.

Term Mortgages are commonly used when:

- Buying your own home to live in

- Acquiring rental properties that are ready to let

- Refinancing to release equity at low cost

Interest rates are lower than for bridging (often 4–6% p.a. in 2025), but the process takes longer. Lenders assess income, credit history, and the condition of the property, so approval can take several weeks or months.

Main Differences at a Glance

When Homebuyers Might Use Bridging

A bridging loan is helpful when you want to buy a new home but haven’t sold your current one yet. It lets you move quickly, avoid losing the new property, and then repay the loan once your old home is sold.

Bridging can also help with properties that aren’t currently habitable (e.g., no bathroom or kitchen) which mortgage lenders typically reject. Once the property is made habitable, you can switch to a term mortgage. However, the costs of bridging are higher, and there’s risk if your sale or refinance doesn’t happen in time. A clear exit plan is essential.

Bridging for Buy-to-Let Investors

Landlords often use bridging loans for quick purchases and refurbishments. The BRR (Buy, Refurbish, Refinance) model is a common strategy: buy a discounted or unlettable property using a bridge, renovate it, and then refinance with a long-term buy-to-let mortgage.

Bridging is also handy for:

- Auction purchases with fast deadlines

- Properties needing structural work

- Projects where rental income won’t cover mortgage affordability until after renovation

The key is to plan the refinance or sale carefully. If delays or valuation issues arise, profit margins can be hit due to high monthly interest.

Bridging Loans for Developers

Bridging finance is useful for property developers in two main ways:

- Exit Finance – Once a project is complete, a developer may use a bridge to repay development funding and give time to sell units without pressure. This reduces costs and avoids rushed sales.

- Refurbishment Projects – Developers tackling major refurbishments or conversions often use bridging to fund both the purchase and renovation before exiting with a mortgage or sale.

Bridging allows developers to move faster than traditional finance allows, but the costs are high and timing is critical. Having a plan B (like refinance or investor support) is wise.

Current Market Trends (2024–2025)

The UK bridging loan market is thriving. In 2024, lending volumes hit a record £7.34 billion, up 27% from the year before. Forecasts suggest it could reach £9 billion in 2025. This growth is driven by:

- More auction purchases

- Slow mortgage processing

- Developers needing exit finance

- Buyers wanting to avoid broken chains

Bridging is also becoming faster. Average completion times dropped to under 50 days, with some cases completing in under two weeks.

Rates have stayed fairly stable. Average bridging rates in 2024 were around 0.88% per month, while top borrowers now access rates as low as 0.55%. Meanwhile, mortgage rates (which had jumped above 6%) have started to ease with base rate cuts in 2025.

Which Option Is Right for You?

Choose bridging finance if:

- You need money fast to secure a deal

- You’re buying a property not eligible for a term mortgage

- You have a clear and reliable exit plan (e.g. sale or remortgage)

Choose a traditional term mortgage if:

- You’re buying a standard home or rental for the long term

- The property is ready to live in or rent out

- You want lower interest costs and predictable payments

In some cases, using both can work well: bridge for the initial purchase, then switch to a term mortgage when ready.

Final Word

In today’s fast-moving property market, knowing when to use a bridging loan or a term mortgage can give you a real advantage. Bridging finance is no longer just for experienced investors – it’s now a flexible tool for homebuyers and newer developers too. Just make sure you understand the risks and have a solid repayment plan. When used smartly, bridging can open doors that a traditional term mortgage can’t.